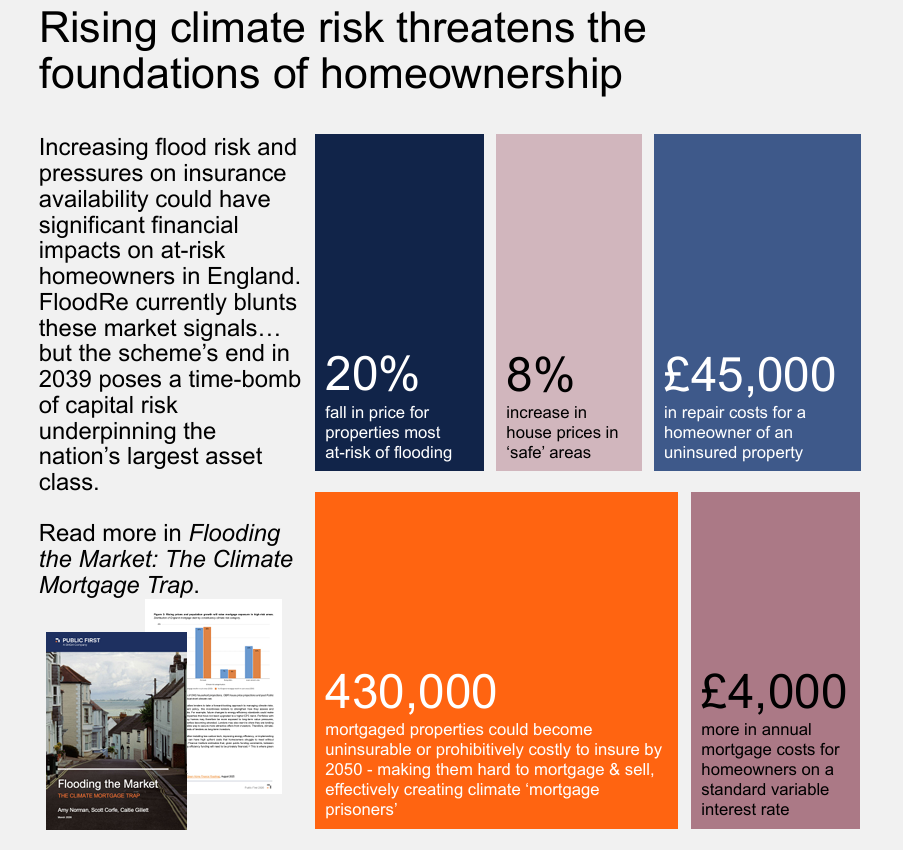

Flooding the Market: The Climate Mortgage Trap

Our new report with Public First has found that hundreds of thousands of households in England could become “climate mortgage prisoners” due to flooding. The paper, titled Flooding the Market: The Climate Mortgage Trap, shows that the owners of 430,000 homes, equivalent to the size of Birmingham, could fit this category by 2050.

You can read the full report here.

The report analyses how rising risks of river, sea and surface water flooding could cause property insurers to increase their premiums or withdraw their coverage altogether. This will leave increasing numbers of homeowners with little choice but to accept more expensive standard variable rate (SVRs) mortgages when their fixed-term periods end.

Households may also face costs of up to £45,000 to make their homes liveable after a storm due to their climate exposure, while being uninsured. These properties would be hard to sell as they cannot be mortgaged or remortgaged and are unappealing to outright cash buyers.

Stuck paying exorbitant interest payments and footing mounting repair bills, they risk becoming “climate mortgage prisoners”.

Large numbers of mortgage prisoners in communities could disrupt the flow of lending and create a localised credit crunch, putting pressure on financial services, the authors warn. This may result in extended selling periods and depressed sale prices, increasing loss-given default and triggering collateral write-downs on lenders’ balance sheets.

In a future worst-case scenario, where losses become widespread and banks’ profitability and resilience are heavily impacted, the authors say market shocks could “cascade through the wider financial system, posing a risk to overall financial stability.”

We put forward several recommendations to protect both homeowners and the wider financial system. These include mandating Flood Performance Certificates (FPCs) for homes, before expanding this to cover Resilience Performance Certificates (RPCs), and to build property-level flood resilience (PFR) measures in high-risk areas.

We also urged ministers to confirm re-insurance scheme FloodRe’s future by the end of the parliament, giving insurers and lenders certainty ahead of its 2039 closure. This would avoid a cliff-edge, where high-risk homes become uninsurable and un-mortgageable.

Our report suggests that the government should be boosting green mortgage uptake and prepare the market for future resilience mortgages. Policymakers should also consider new ways to strengthen planning policy and building regulations to support property-level flood resilience measures.

More broadly, the government should strengthen and accelerate the UK’s climate adaptation strategy, ensuring this is integrated across relevant government policy objectives – such as bringing together natural flood management and farming policy.